Factor investing in the news reached a high last quarter

(Google trends)

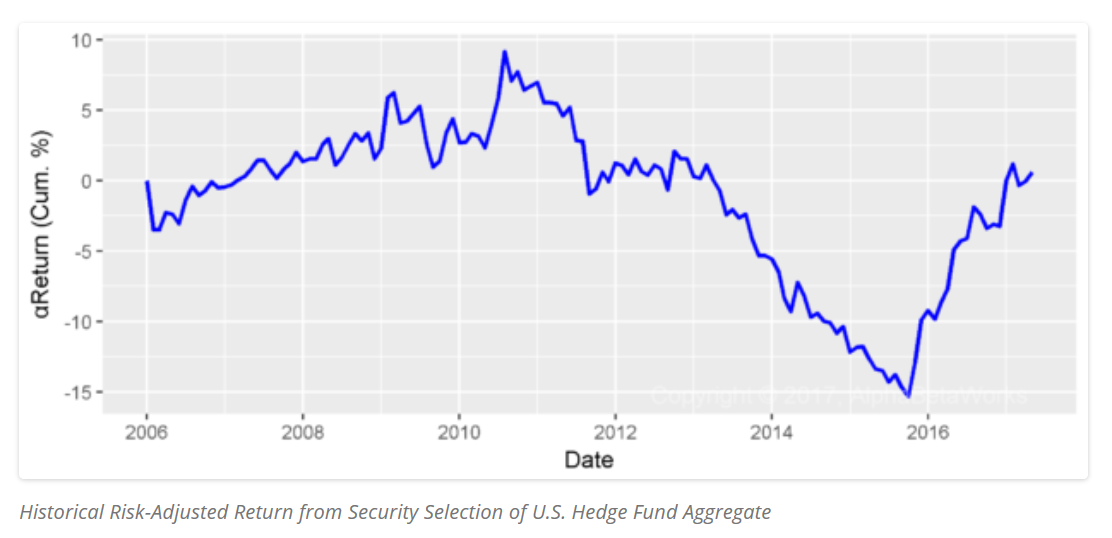

Below graphs (courtesy ab insights) show crowed hedge funds factor bets (equities) started underperforming in 2011 and accelerated since 2015

For other asset classes we see similar trends with CTA inflows the highest in 2016 and poorest performance in the last 15th months

Many reasons are coming out for the underperformance of factor investing and more broadly quant strategies, some you can find in a recent article by Neal Berger https://www.linkedin.com/pulse/turmoil-quant-land-hedge-funds-candid-view-why-strategies-knab

Obviously not all factor investing is done properly and quant strategies mean many things so ask more questions as you allocate.

Now, global macro and discretionary has bad press recently, I wouldn't be surprised to see them outperforming from here as central banks and regulatory environment is taking a back seat, and discretionary traders start using the enormous new open source techniques at their disposal.

No comments:

Post a Comment