Largest straight decline in 5yrs moving 57bps in the last couple weeks

We see a similar picture in CAD 2y yields differentials and CAD currency

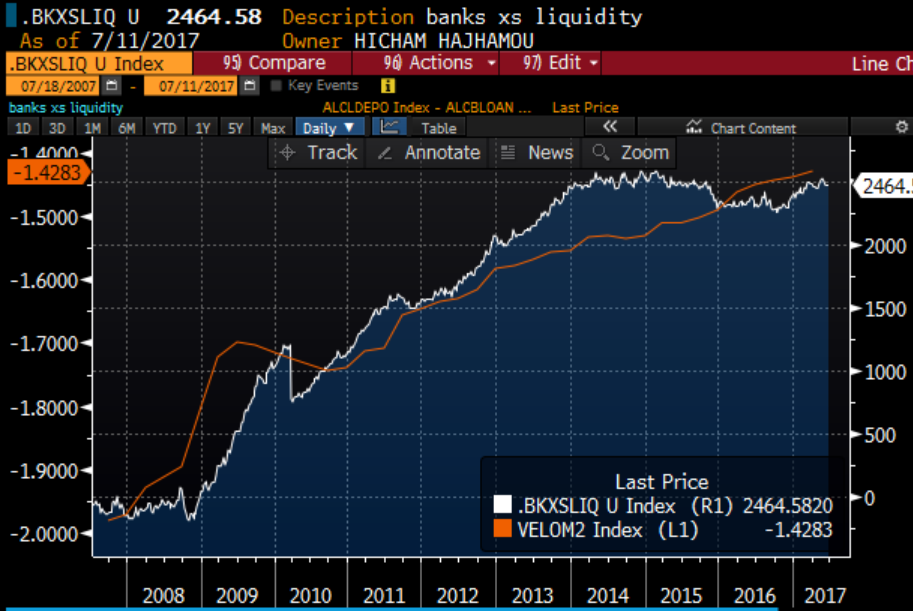

Below is the 3months Libor/OIS spread showing some more stress in the system

The recent move was therefore justified by many macro variables, heating housing market, higher credit risk, a bounce in commodity markets...forcing a change in monetary policy with central bank raising rates

This is confirmed by my global macro model.

Long term model targets a 10y differential at 29bps so pretty close to current 26bps market level, while shorter term model shows a spread at 38bps.

So if short term dynamics are stretched, Z-scores measures are not at less than 1 standard deviation

I still believe move was too fast and worth buying 10y CAD vs 10y US into US supply next month for trade.